Collaboration, Competition, and Conflict – Moneyweb

The first formal agreement between the United States and China was forged in 1844 under questionable circumstances. After Britain made significant advancements from the Qing Empire in the First Opium War, the United States aimed for equally favorable terms.

This led to the Treaty of Wangxia, which was signed between a rising power, the US, and a declining one.

The treaty allowed the US access to five treaty ports (Guangzhou, Xiamen, Fuzhou, Ningbo, and Shanghai), where Westerners received special privileges, including extraterritoriality. This particularly infuriated the Chinese, as it meant that Westerners accused of crimes could evade being tried by Chinese authorities.

Read:

The new superpower test: Who is trusted when fear rises?

Winners and losers from Trump and Xi’s two-day Beijing summit

This initiated an era known in China as the “century of humiliation,” marked by a second Opium War, a Japanese invasion, civil war, and the communist revolution in 1949.

In stark contrast, last week’s meeting between Presidents Donald Trump and Xi Jinping in Beijing was held in a more amicable environment, leading to mutual declarations of support and collaboration.

Nevertheless, substantial underlying tensions still exist.

At present, China is the emerging competitor challenging the US’s status as the sole global superpower. China has robust ties with Russia and opposes Western backing for Ukraine, while being the leading customer of Iran.

Taiwan is a significant point of conflict, with China firmly advocating for eventual reunification, while the US supports maintaining the current status quo.

The key role Taiwan plays as the world’s leading producer of advanced semiconductors positions it at the center of the artificial intelligence (AI) boom, complicating the situation further.

Read:

Taiwan market cap tops $4trn on AI boom, overtaking UK

Global chip stocks soar as Huang helps fuel AI euphoria at Davos

The US has been working to preserve its lead in AI and other technologies by limiting China’s access to high-end chips. Conversely, China leads in several technologies related to the green transition, being the largest producer of solar panels, batteries, wind turbines, and electric vehicles.

Essentially, it resembles the Saudi Arabia of clean energy, and given that AI demands substantial electricity, this might ultimately provide it with a competitive advantage.

China also controls 80% to 90% of the global supply of numerous “rare earth” minerals, vital for various military and industrial technologies, granting it significant leverage in discussions with any nation, including the US.

The world’s factory

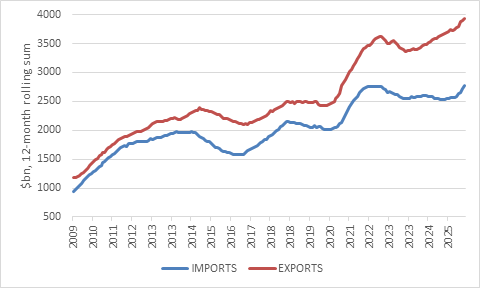

Indeed, China is overwhelmingly the largest producer of many goods—both basic and advanced—that are essential to global markets. Consequently, its trade surplus (exports minus imports) has reached unprecedented levels, exceeding $1 trillion last year.

This narrative reverberates with historical echoes.

The Opium Wars forced China to tolerate drug imports from Britain and other colonial forces.

Read:

US-China trade truce leaves fundamental issues unresolved

A Supreme Court showdown looms for Trump’s tariffs

China faces contradictions

While the Western world craved Chinese products, that desire was not reciprocated, resulting in a significant outflow of gold and silver eastward [China accepted payment only in precious metals]. Compelling China to import opium under threat—a tactic employed after colonial powers ensnared its population in addiction—had catastrophic social repercussions and served as a strategy to rectify the drastic trade imbalance.

Similarly, Trump imposed tariffs on China during his first term to counter the modern trade deficit, a stance largely echoed by his successor, Joe Biden.

Hardline attitudes toward China have become a rare bipartisan issue in Washington.

During his second term, Trump escalated these efforts, once imposing tariffs on Chinese goods as high as 145%. After negotiations, exemptions, and ultimately intervention from the Supreme Court, the effective tariff on Chinese imports now stands at around 25%, considerably elevated compared to previous levels.

ADVERTISEMENT

CONTINUE READING BELOW

Consequently, exports from China to the US have dropped significantly. At its peak in 2017, almost a quarter of US imports by value came from China.

As of April this year, that figure has plummeted to merely 8%, although a substantial quantity may still be rerouted through third countries like Vietnam.

While many nations have not mirrored Trump’s approach of increasing trade barriers against China, it does not indicate a lack of eagerness to do so.

China’s exports and imports by value

Source: LSEG Datastream

This remarkable export strength, combined with the relative decline in imports, suggests a shift towards domestic brands.

However, the trade surplus also highlights a weakness: a lack of domestic demand. This is partly a deliberate choice.

As is well-known, China’s economic model structurally prioritizes investment over consumption, resulting in households receiving a smaller share of national income in comparison to nations at a similar developmental stage.

Meanwhile, significant resources were invested in constructing world-class infrastructure and manufacturing capabilities. Yet, a large portion of this investment was directed toward residential real estate, culminating in a massive bubble that burst in 2022.

The fallout from the property bubble continues to echo throughout the economy. A drop in apartment sales leads to fewer purchases of refrigerators, televisions, and beds—many of which would have been imported.

If imports had matched exports, Chinese consumers could have had an additional $100 to $200 billion worth of foreign goods.

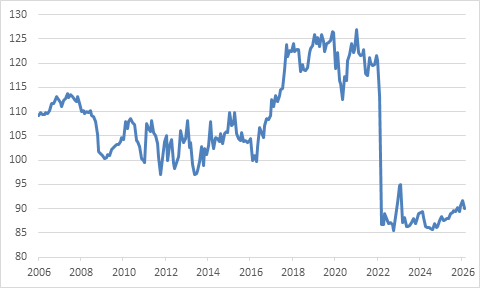

Instead, consumer confidence remains historically low, though it has slightly improved from a year ago.

Chinese consumer confidence

Source: LSEG Datastream

Yuan too few

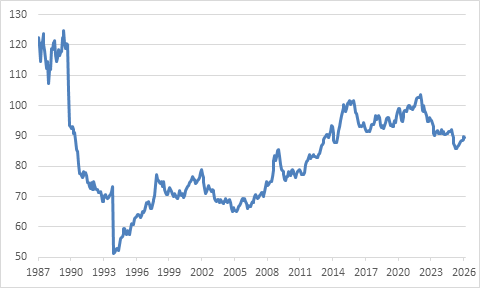

Another reason for the weakness in imports—and strength in exports—is an undervalued currency, a long-standing grievance from the US government.

A nation with such a significant trade surplus would generally experience upward pressure on its currency. Despite some recent appreciation, the yuan remains relatively weak on a real trade-weighted basis.

China real trade-weighted exchange rate

Source: OECD

A devalued currency tends to boost exports and limit imports, which is why Trump advocates for a softer dollar and a stronger yuan.

ADVERTISEMENT:

CONTINUE READING BELOW

A transition like this would help balance the trade relationship between China and the rest of the world, while enhancing the purchasing power of Chinese households, allowing for increased access to foreign goods, services, and international travel.

The yuan’s exchange rate is overseen by the People’s Bank of China (PBOC), making its level a conscious decision rather than a simple outcome.

While it may be wise for the yuan to gradually appreciate over time, the PBOC has historically prioritized stability above all else.

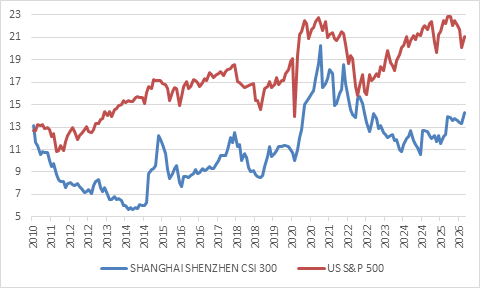

Now, we compare equity markets between the US and China. Although China can confidently present itself as an economic, military, and technological superpower, market valuations reveal a different narrative.

In contrast, despite discussions of a US decline during Trump’s unpredictable presidency, the S&P 500 has consistently reached new record heights, even amid ongoing geopolitical strains.

Forward price-earnings ratios

Source: LSEG Datastream

Chinese equities are trading at a substantial discount compared to US counterparts, particularly considering that the yield on a 10-year US government bond was just below 4.5% last week, while China’s equivalent stood at only 1.7%. This points to a significant ‘equity risk premium’ in Chinese stocks, whereas US equities exhibit little margin for safety.

Some of this discrepancy can be attributed to unpredictable regulatory changes that led to China being labeled as “uninvestable” around 2021. However, since then, authorities have shifted their approach toward Chinese equity markets.

Historically, Beijing has perceived equity markets as secondary, prioritizing economic development funding through the banking system over speculation. However, banks are now constrained by a struggling property sector, while the successes of other nations—especially the US tech sector—have illustrated how equity markets can foster innovation and business growth while also generating wealth for families, crucial in a country facing an aging population and uneven social security coverage.

Thus, regulators now aim to foster a “slow bull market” through steadily increasing equity values to stimulate economic growth and assist Chinese families in saving for retirement.

To achieve this, corporate governance standards have been enhanced, and publicly listed companies are encouraged to provide regular dividends, marking a much-needed transition toward a more shareholder-friendly framework.

Despite China’s impressive economic accomplishments, publicly traded firms have struggled to convert GDP growth into profit growth, leading to mediocre equity returns. Conversely, the primary reason the S&P 500 enjoys a premium likely stems from its reliable earnings per share growth, outpacing other significant markets.

The profitability of China’s industrial companies has been further undermined by overcapacity and intense competition, challenges policymakers are addressing through “anti-involution” initiatives.

For investors outside of China, the blend of a depreciated currency, low valuations, and increased policy support is likely appealing.

China’s representation in major global equity indices compiled by firms like MSCI and FTSE Russell has decreased to about 3%, disproportionate to its contribution to global economic output and innovation.

Despite this, risks remain.

China’s adverse demographic situation is widely acknowledged, primarily due to the now-repealed one-child policy. Last year recorded only 7.9 million births, the lowest figure since the Communist Party came to power in 1949.

ADVERTISEMENT:

CONTINUE READING BELOW

Read: China’s population grew older and richer … [Jun 2023]

While life expectancy has significantly increased—now surpassing that of the US, a remarkable achievement—this doesn’t alleviate the workforce contraction and will undoubtedly limit long-term GDP growth rates (again, for equity investors, profits are more crucial than GDP).

This trend may also prompt innovation and technological adoption.

According to the International Federation of Robotics, China accounted for half of the world’s industrial robot installations in 2024, with most supplied by domestic companies for the first time.

China’s approach to artificial intelligence appears focused on practical applications rather than pursuing bleeding-edge models, standing in contrast to Silicon Valley’s winner-takes-all mentality.

Time will tell which strategy proves more effective.

Total debt-to-GDP ratios

Source: Bank for International Settlements

A significant concern is the elevated total debt levels (including household, government, corporate, and financial sectors), which surpass those of the US when measured as a percentage of GDP. Notably, the speed at which this debt has grown is clearly unsustainable.

China boasts a far higher savings rate than the US or any other large economy, with most of its debt being domestically held.

Thus, the core issue relates more to internal distribution rather than existential threats. Nonetheless, in a slowing economy, servicing this debt poses challenges, and someone must shoulder the resulting losses.

A significant risk lies in the US-China dynamic.

Both nations are actively seeking to reduce dependency on each other, with China possibly at an advantage. However, their economies remain deeply interconnected, rendering the idea of complete decoupling unrealistic.

As a result, a sudden rupture over Taiwan or other flashpoints could lead to a substantial market drop, affecting global markets well beyond just China.

If the US were to impose sanctions against China, any financial institution would need to comply or face isolation from the dollar system.

In this regard, the US retains considerable leverage, as China is well aware.

Such a conflict would harm all parties involved, making last week’s summit between Trump and Xi particularly significant, even if it resulted in no groundbreaking policy changes or resolutions to contentious issues.

Read:

China will open its market to AI chips from the US, Nvidia’s CEO says

Xi urges Hormuz reopening in rare call with Saudi de facto ruler

US says China agrees to spend billions on agricultural goods

While cordial gestures don’t resolve deep-rooted disagreements, they help maintain open lines of communication. The strategic rivalry between the world’s superpowers is inevitable, but it can be managed.

Ultimately, both sides—and the globe—stand to lose if this rivalry escalates into overt conflict.

Izak Odendaal is an investment strategist at Old Mutual Wealth.